UBS Hikes Micron Price Target to Street-High $1,625 as Memory Supercycle Accelerates

Main Takeaway

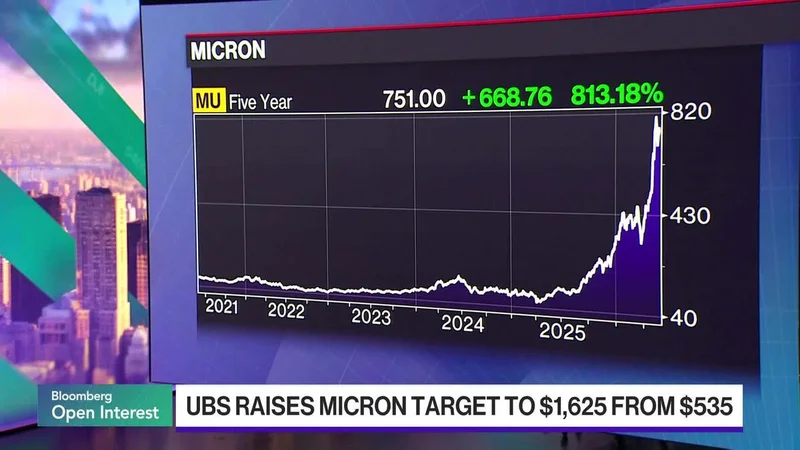

UBS raised Micron's price target to $1,625, the highest on Wall Street, as the chipmaker's market cap surged past $1 trillion on AI-driven DRAM demand.

Jump to Key PointsSummary

What triggered the latest rally

Micron Technology shares jumped 18.7% on May 26, 2026, hitting a new 52-week high of $892.10 and pushing the company's market capitalization past $1 trillion for the first time. The surge came after UBS raised its 12-month price target to $1,625, more than triple its previous target of $535 and the highest on Wall Street. Trading volume reached 42.6 million shares, nearly double the 10-day average, according to CNBC data.

The upgrade reflects intensifying demand for high-bandwidth memory (HBM) used in AI accelerators, where Micron has secured supply agreements with major chip designers. UBS analyst Timothy Arcuri cited a deepening shortage of dynamic random access memory (DRAM) chips and rising demand across multiple sectors as core drivers. The firm maintained its buy rating, projecting Micron's market value could more than double to $1.8 trillion within 12 months.

How Micron's valuation transformed in 12 months

Micron's market cap has soared approximately 700% over the past year, transforming the Idaho-based chipmaker from a mid-tier semiconductor player into one of America's 10 most valuable technology companies. The stock traded as low as $92.22 in May 2025, meaning investors who bought at the bottom have seen nearly a tenfold return. As of May 26, 2026, the company commands a $1.005 trillion valuation with a beta of 1.99, indicating significantly higher volatility than the broader market.

This dramatic repricing stems from a structural shift in memory demand. AI training and inference require vastly more memory bandwidth than traditional computing workloads. Micron's HBM3E products, which stack memory dies vertically to increase data throughput, now command premium pricing and long-term supply contracts. CEO Sanjay Mehrotra has positioned the company's manufacturing expansion, including its new facility in Clay, New York, to capture this demand wave.

Why UBS calls this a memory supercycle

UBS's supercycle thesis rests on supply constraints that defy traditional semiconductor cyclicality. In April 2026, the firm had already raised its target to $535 from $510, arguing that negative sentiment around Micron's gross margin guidance missed the bigger picture. The May upgrade to $1,625 represents a radical acceleration of that view, implying the cycle has strengthened beyond prior expectations.

The investment bank's analysis points to several factors breaking historical patterns. Memory capital expenditure has been suppressed for years following the 2022-2023 downturn, leaving insufficient supply to meet AI-driven demand. Meanwhile, HBM's complex 3D stacking technology creates higher barriers to entry, concentrating market share among Micron, Samsung, and SK Hynix. UBS believes these dynamics will sustain elevated pricing for multiple years rather than the typical 12-18 month upcycle.

The competitive landscape for AI memory

Micron's surge places it in direct competition with Samsung and SK Hynix for dominance in the HBM market, which supplies NVIDIA, AMD, and custom AI chip programs. While Samsung holds the overall memory revenue lead, Micron has gained traction with NVIDIA's latest Blackwell-generation accelerators. The three-company oligopoly means market share shifts can produce outsized financial impacts.

Supply agreements in HBM typically span 2-3 years with fixed pricing, creating revenue visibility rare in commodity memory markets. This shift from spot-market exposure to contracted revenue streams justifies the higher valuation multiples investors now assign to Micron. The company's U.S. manufacturing footprint also provides geopolitical risk mitigation for customers concerned about Taiwan Strait tensions, where much advanced memory packaging occurs.

Risks that could derail the bull case

Despite the euphoric price action, several factors could challenge UBS's $1,625 target. Micron's beta of 1.99 means the stock amplifies any broader market downturn, and its 52-week range, $92.22 to $892.10, demonstrates extreme volatility. A memory demand slowdown, whether from AI capital expenditure cuts or macroeconomic weakness, would hit Micron disproportionately.

Geopolitical tensions also remain relevant. While easing Middle East tensions contributed to the May 26 rally, the U.S.-China technology rivalry and potential export restrictions on advanced memory to Chinese customers pose ongoing risks. Additionally, Samsung and SK Hynix are expanding HBM capacity aggressively, which could eventually erode pricing power. UBS acknowledges these risks but argues the current supply-demand imbalance is severe enough to sustain the supercycle thesis through at least 2027.

What investors should watch next

Micron's next quarterly earnings report, expected in late June, will test whether the company can meet the lofty expectations embedded in its trillion-dollar valuation. Analysts will focus on HBM revenue mix, average selling price trends, and capital expenditure guidance for fiscal 2027. The company's ability to execute on its Clay, New York facility timeline will also weigh on long-term supply assumptions.

Wall Street's consensus target will likely shift higher following UBS's move, though the $1,625 figure remains an outlier. Whether Micron can approach that level depends on sustaining the current pricing environment while scaling HBM production without the yield issues that have plagued competitors. For now, the stock's 124% year-to-date gain suggests investors are pricing in a prolonged period of exceptional profitability.

Key Points

UBS raised Micron price target to $1,625, highest on Wall Street

Micron market cap surpassed $1 trillion after 18.7% single-day surge

Stock has gained 700% over past 12 months on AI memory demand

HBM3E supply agreements with AI chipmakers drive revenue visibility

Memory supercycle thesis defies traditional semiconductor cyclicality

Questions Answered

UBS cited a deepening DRAM shortage, AI-driven HBM demand, and a memory supercycle defying traditional cyclicality, leading it to more than triple its target to $1,625.

Micron shares rose 18.7% on May 26, 2026, and have gained approximately 700% over the past 12 months and 124% year-to-date.

Artificial intelligence training and inference require high-bandwidth memory (HBM), where Micron's 3D-stacked HBM3E products supply NVIDIA, AMD, and other AI chipmakers.

Samsung and SK Hynix compete with Micron in the HBM market, forming a three-company oligopoly with high barriers to entry due to complex 3D stacking technology.

Key risks include AI capital expenditure cuts, macroeconomic weakness, Samsung and SK Hynix capacity expansion, and potential U.S.-China technology export restrictions.

Investors should focus on HBM revenue mix, average selling price trends, capital expenditure guidance for fiscal 2027, and progress on the Clay, New York manufacturing facility.

Source Reliability

60% of sources are trusted · Avg reliability: 73

Go deeper with Organic Intel

Simple AI systems for your life, work, and business. Each one includes copyable prompts, guides, and downloadable resources.

Explore Systems