ASML's 42% Stock Surge Leaves It Cheaper Than U.S. Chip Peers

Image: Bloomberg AI

Main Takeaway

ASML shares hit record highs after surging 42% in a month, yet its forward valuation gap with U.S. peers hit a decade low.

Jump to Key PointsSummary

Why ASML looks cheap despite record prices

ASML Holding NV's stock has climbed to fresh all-time highs, delivering a 41.9% surge in the past month and a 47.1% year-to-date gain according to Sahmcapital. Yet this eye-catching rally has failed to lift its relative valuation against American semiconductor peers. Bloomberg reports that the gap between ASML's forward price-to-earnings ratio and those of U.S. competitors has widened to its most extreme level in years. The Dutch lithography giant now trades at a significant discount despite its irreplaceable role in producing the most advanced chips. This creates a puzzle for investors: a company with a technical monopoly on extreme ultraviolet (EUV) machines that costs more than $200 million each, yet priced like it is running behind.

The disconnect stems partly from geographic and regulatory risk. ASML is headquartered in Europe, subject to export controls on its most sophisticated systems, and exposed to China trade tensions that U.S.-based Nvidia or Applied Materials face less directly. Markets appear to be pricing in a persistent uncertainty premium that has kept ASML's multiple compressed even as order books swell.

How the valuation gap reached a decade low

Bloomberg's analysis highlights that ASML's forward P/E has dropped to its lowest level relative to U.S. semiconductor peers in approximately ten years. This is not a subtle divergence. The stock's cheapest relative valuation in years coincides with record absolute prices, a combination that defies typical market behavior where strong momentum usually drags multiples higher. Sahmcapital notes that over five years, ASML has delivered 181.5% returns, yet this long-term wealth creation has not translated into valuation respect versus faster-growing or more aggressively priced American alternatives.

The compression reflects a broader market preference for U.S. tech narratives. Investors have poured capital into Nvidia's AI infrastructure story and AMD's turnaround, while treating ASML as a capital equipment vendor rather than a critical enabler of the entire semiconductor roadmap. Simply Wall St's valuation scoring rates ASML poorly on peer-relative metrics, with its price-to-earnings ratio sitting below fair value estimates on multiple measures. This suggests the discount is measurable, persistent, and not merely a perception gap.

What is driving the recent share price momentum

The 32.5% to 42% monthly surge, depending on measurement period, comes as semiconductor demand rebounds across multiple end markets. Webull reports that big chipmakers are securing cutting-edge equipment orders, and ASML's unique position as the sole producer of EUV lithography systems gives it unmatched pricing power. The company has effectively zero competition for its most advanced machines, a monopoly that typically commands premium valuations in industrial markets.

Yet the rally may also reflect catch-up dynamics. ASML had underperformed through much of 2024 and early 2025 as investors worried about China export restrictions and cyclical downturns in memory and logic chip spending. The recent surge could represent recognition that these fears were overstated, or that AI-driven capital expenditure will sustain demand regardless of regional headwinds. Chartmill's fundamental data shows the stock trading around 1,499 EUR, with recent sessions seeing modest pullbacks that suggest some profit-taking after the rapid ascent.

The China export control overhang

A critical factor in ASML's valuation discount is its exposure to Chinese market restrictions. The company faces some of the most complex export control regimes in global technology, with the U.S. government pressuring the Dutch government to limit sales of advanced systems to Chinese customers. This creates revenue uncertainty that U.S. peers with more domestic-focused sales bases do not encounter to the same degree. Bloomberg's reporting emphasizes that this geopolitical risk premium is a persistent drag on how investors price ASML shares.

The irony is that restrictions may actually strengthen ASML's long-term position. If Chinese domestic lithography efforts fail to mature, global chipmakers using ASML equipment gain competitive advantage. If they succeed, ASML loses a market but retains technological leadership elsewhere. The market appears to be pricing the worst case, where Chinese competition emerges and Western markets simultaneously slow. This double-pessimism may explain why even record stock prices leave the valuation multiple lagging so far behind American peers.

What investors are weighing for the next move

The investment case hinges on whether ASML's valuation gap represents a buying opportunity or a warranted discount. Bulls point to the company's irreplaceable technology, expanding AI-driven demand for advanced chips, and a five-year track record of 166.5% to 181.5% returns. Bears counter that regulatory risks are structural, not temporary, and that U.S. peers offer purer plays on AI growth with fewer geopolitical complications. Simply Wall St's fair value analysis suggests the stock trades below future cash flow estimates, implying upside if execution continues.

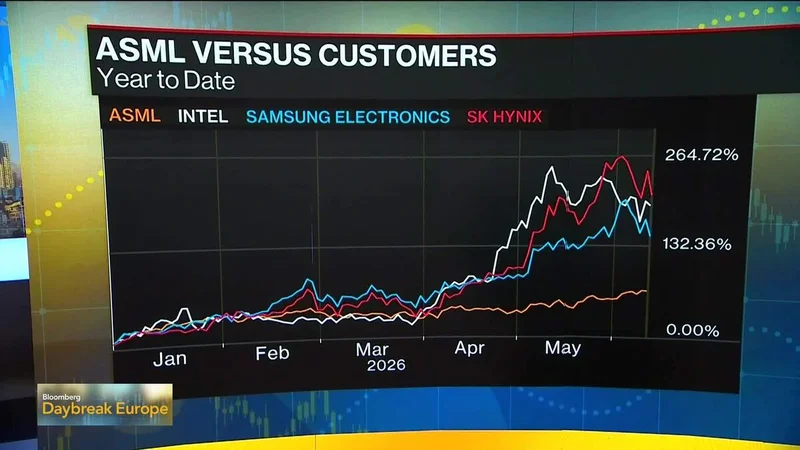

The near-term catalyst will be order flow and guidance. If major customers like TSMC, Samsung, and Intel accelerate EUV purchases for 2nm and below process nodes, ASML's revenue visibility improves and the valuation gap could narrow rapidly. If macroeconomic concerns or further China restrictions emerge, the discount may persist or deepen. For now, the market has spoken clearly: it will pay more for semiconductor stories it finds simpler, even when the fundamentals point toward the more complex one.

How ASML compares to its American rivals

The peer comparison reveals the starkness of ASML's valuation position. U.S. semiconductor equipment makers and chip designers trade at substantial premiums, reflecting investor comfort with domestic policy, larger addressable market narratives, and aggressive growth expectations. ASML's revenue concentration in a few massive machines per quarter creates lumpy results that momentum investors dislike, even as the long-term contracts provide more visibility than many software businesses.

Webull's analysis frames the choice facing investors as whether to chase the momentum in U.S. names or capture what may be a rare discount in a structurally dominant company. The 32.5% monthly surge suggests some investors are making that switch. Whether this re-rating continues depends on ASML's ability to convert its technical monopoly into the kind of narrative that commands premium multiples in today's market. That has historically been the harder challenge for European technology champions operating in an American-dominated investment landscape.

Key Points

ASML stock surged 41.9% in one month to record highs while forward P/E hit decade low versus U.S. peers.

The valuation discount reflects China export restrictions and European geographic risk premium.

ASML holds monopoly on EUV lithography machines costing over $200 million each.

Simply Wall St rates ASML's peer-relative valuation at 1/6, indicating significant undervaluation.

AI chip demand and 2nm node transitions could drive order acceleration and re-rating.

Questions Answered

ASML trades at its cheapest relative valuation in years against U.S. peers despite record stock prices. The discount stems from China export control exposure, European headquarters, and investor preference for American tech narratives over capital equipment stories.

ASML shares gained approximately 41.9% in the past month and 47.1% year-to-date according to Sahmcapital, reaching fresh all-time highs around 1,499 EUR per share.

ASML is the sole producer of extreme ultraviolet lithography systems, which are required to manufacture the most advanced chips at 2nm and below. Each machine costs over $200 million and has no competitive equivalent.

China restrictions create revenue headwinds but ASML's core growth driver is AI-fueled demand from Western and Taiwanese chipmakers. The company maintains technological leadership that Chinese domestic alternatives cannot yet match.

Accelerated EUV orders for advanced AI chips, sustained order growth from TSMC and Intel, or reduced geopolitical uncertainty could trigger re-rating. The gap is historically wide, suggesting asymmetric upside if sentiment shifts.

Source Reliability

57% of sources are established · Avg reliability: 60

Go deeper with Organic Intel

Simple AI systems for your life, work, and business. Each one includes copyable prompts, guides, and downloadable resources.

Explore Systems